8.6 Measurement and Verification

8.6.1. Measurement & Verification (M & V)

Measurement and Verification is a process of quantifying energy consumption before and after an energy conservation measure is implemented in order to verify and report on the level of savings actually achieved.

M&V activities commonly form the basis for savings verification in Energy Performance Contracts and operate for a defined term as established by the contract. The central purpose of M&V is to verify the energy savings achieved by building retrofits, either to satisfy internal financial accounting and reporting requirements, or to meet the terms of third-party contracts for project implementation and management.

8.6.2. M & V Protocols

Measurement & Verification (M&V) protocols provide a framework and options for determining energy savings. The most widely used protocol internationally are the ff:

- IPMPV

International Performance Measurement and Verification Protocol (IPMVP). It provides four options for determining energy savings: retrofit isolation, key parameter measurement; retrofit isolation, all parameter measurement; whole facility; and calibrated simulation. The IPMVP is published by the Efficiency Valuation Organization (EVO) in three volumes.

- ASHRAE Guideline 14-2002

The other M&V protocol used in the United States is the ASHRAE Guideline 14 Measurement of Energy and Demand Savings. These guidelines have three M&V options, which are the same as the IPMPVP, less the key parameter measurement option. ASHRAE Guideline 14 is more technical than the other protocols, but the fundamental principles of M&V are the same for all three protocols.

8.6.3. Why Measure and Verify

M & V is an additional cost in the retrofit project—what is the payoff?

The IPMVP offers six answers to this question:

- M & V increases energy savings.

- M & V reduces the cost of financing projects.

- M & V encourages better project engineering.

- M & V helps to demonstrate and capture the value of reduced emissions from energy efficiency and renewable energy investments.

- M&V increases public understanding of energy management as a public policy tool.

- M & V helps organizations promote and achieve resource efficiency and environmental objectives.

Spend more to reduce costs? . . . This isn’t a contradiction in terms. The IPMVP explains that a thorough M & V process designed into the project helps to reduce the total cost of a financed project by:

- Increasing the confidence of funders that their investments will result in a savings stream sufficient to make debt payments

- Thereby reducing the risk associated with the investment

- Thereby reducing the expected rate of return of the investment—and your costs of borrowing.

8.6.4. General Approach to M & V – The IPMVP

In principle, M&V simply quantifies energy savings by comparing consumption before and after the retrofit. The “before” case is defined as the “baseline performance”, and the “after” case is referred to as the post-installation period. In its simplest form,

The complicating factors concern:

- What adjustments to the Baseline performance are required, and how are they carried out;

- What measurements are required to determine post-installation performance, and how are they carried out.

The International Performance Measurement & Verification Protocol (IPMVP), published by the US Department of Energy, defines four approaches to M&V that determine how these factors are addressed. These approaches are termed M&V Options A, B, C and D. A critical decision in M&V planning is the selection of one of these options.

8.6.5. M & V Options

IPMVP M&V Options A, B, C and D are summarized below. They differ one from another in terms of:

- The degree to which the retrofit can be measured separately from other facility components;

- The extent to which performance variables can be measured.

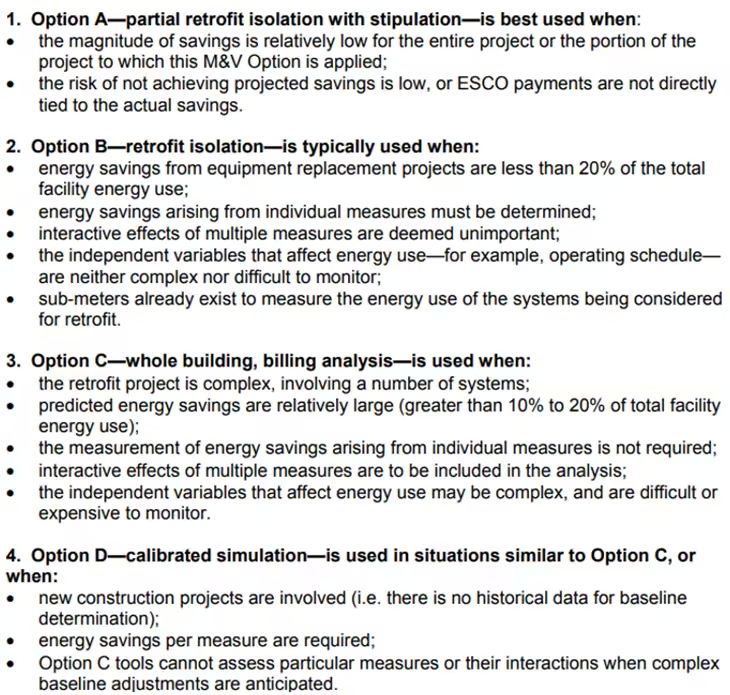

Option A (Partial Retrofit Isolation with Stipulation)

Option A applies to a retrofit or system level assessment where performance or operational factors can be spot or short-term measured during the baseline and post- installation periods. Factors that cannot or are not measured are “stipulated”, based on assumptions, analysis of historical performance, or manufacturer’s data. Stipulation is the easiest and least expensive method of determining savings, but is also subject to the greatest level of uncertainty.

Option B (Retrofit Isolation)

Option B applies to a retrofit or system level assessment where performance or operational factors can be spot or short-term measured at the component or system level during the baseline and post-installation periods. In this Option, the performance of the retrofit can be measured separately from other measures or performance factors. No factors are stipulated; consequently, Option B involves more end-use metering than Option A and is correspondingly both more expensive and less subject to uncertainty.

Option C (Whole Facility Option)

Option C applies to the impact of a “bundle” of retrofit measures on a facility. It relies on baseline and post-installation total building energy performance data typically obtained from the utility meter at the service entrance, and involves regression analysis against independent performance variables such as weather factors, facility usage, or production (as in water pumping stations or wastewater treatment facilities).

Option D (Calibrated Simulation)

Option D uses computer simulation models of component or whole-building energy consumption to determine project energy savings. Simulation inputs are linked to baseline and post-installation conditions; some of these inputs may be determined from performance metering before and after the retrofit. Long-term whole-building energy use data may be used to calibrate the simulation models.

8.6.6. A Quantitative Basis for M & V

Performance Model

The performance model of energy consumption is developed based upon the existing historical data and knowledge of the energy consuming systems present. The techniques used to develop a performance model for M&V are essentially the same as those statistical techniques used to develop the relationship between energy and its drivers in the practice of M&T described in section 3. In M&V this practice is often referred to as determination of the energy consumption baseline or standard. Given this baseline relationship it is possible to make future comparisons to determine changes in energy consumption, taking into account changes in the influencing factors.

Three basic methods exist for establishing a model:

Previous year’s data – simply using last year as a predictor of this year’s consumption. Typically only useful when there are no significant factors of influence.

Regression analysis – a statistical approach based upon historical consumption and the factors of influence.

Simulation model – using complex numerical computer models to simulate the energy consumption.

The most common method for a basic system is regression analysis. This technique determines an equation between the energy and the variable(s) that influence it. As with any statistical technique it must be used carefully. The reliability of the result depends upon the factors chosen and the quality of the data used. The reader is referred to any basic statistics textbook or the HELP function of most common spreadsheets for more background on regression analysis. Section 3 also provides some basic instruction.

For many situations, the performance model will be an equation of the form:

Baseline Energy Use = Base load Energy + Use Factor x Factor of Influence

Most popular spreadsheets can perform this type of analysis.

Baseline Definition

The definition of the baseline conditions involves not only quantifying energy consumption data, but also specifying those factors that affect energy consumption. Data and information required for a complete baseline definition include:

Independent consumption data

- Electricity consumption information—bills and derived information (kW, kVA, PF), meter readings (especially for subsystem measurements), demand profiles;

- Fuel consumption information—bills, monthly consumption profiles, fuel-by fuel data (quantity, calorific value of fuels consumed, etc.);

- Water consumption information

- Other energy sources—e.g. purchased steam, etc.

Independent variable data

- Weather factors—HDD or CDD;

- Facility occupancy or usage data—operating hours, number of patrons, etc.;

- Throughput or production—as in volume of water pumped or wastewater treated;

- Space conditions—set points on heating/cooling systems;

- Equipment malfunctions—records of outages.

Baseline Adjustments

The fundamental relationship for savings verification includes “adjustment” of the baseline performance. Baseline adjustments potentially represent the most contentious aspect of energy performance contracts, and may be the most difficult aspect of savings verification to quantify. Simply put, “adjustment” places the baseline energy performance on a “level playing field” with post-installation performance in terms of those independent variables that affect energy consumption.

ESCOs must specify as part of their M&V plan how they will adjust the baseline if the post-installation operating conditions are different from those used to determine the baseline. These specifications should address the independent variables listed above, as relevant to the project.

The following are examples of baseline adjustments:

Changes in production or weather

Adjustments might include recalculating the baseline consumption rates using post-installation period production and/or weather data (HDD or CDD) based on the mathematical expression of how energy consumption depends on these factors;

Changes in operating schedule or process changes

The real impact of the retrofit project is independent of decreases or increases in operating hours of the facility or system and, therefore, the baseline consumption needs to be scaled up or down to correspond to such changes if any occur; similarly, process changes— or new loads, improved lighting levels unrelated to the retrofit itself, etc.—that may increase energy consumption in the post-installation period must be separated from the post-installation period performance.

Changes in the actual function of the facility

Production space being converted to storage, for example—and their impact on energy performance separate and apart from the retrofit, need to be quantified as adjustments to baseline performance.

The extent to which baseline adjustments need to be considered depends to some extent on the M&V Option being employed:

- Baseline adjustments are less likely to be needed when M&V Option A is being used since many of the performance factors are stipulated.

- Option B or retrofit isolation involves metering of energy consumption pre- and post-installation; non-metered factors that impact on energy performance therefore need to be applied to the measured baseline consumption.

- Option C involves regression analysis to determine a functional relationship between energy consumption and independent variables; adjustment to the baseline performance for changes in these variables is typically carried out by using that functional relationship or performance model.

- Option D accommodates adjustment within the simulation model itself; once calibrated using actual or typical data, no other adjustments should be required.

8.6.7. Calculating Energy Savings

Energy savings cannot be directly measured because they represent avoided energy consumption. A savings calculation is used to compare energy demand before and after an energy conservation measure is implemented:

The baseline energy use must have sufficient data to accurately represent the energy performance before the project. The baseline performance is used to predict how much energy would have been used if the project had not been implemented. The reporting period energy use is subtracted from the baseline to determine the savings. The reporting period should be at least one operating cycle to fully capture the new energy performance. The Adjustments term represents routine and nonroutine adjustments to the energy performance. A routine adjustment would be energy consumption drivers that are expected to change, such as the weather. Non-routine adjustments are changes that do not usually occur, such as a change in facility size.

8.6.8. Financing Energy Projects

- Equity

Using in-house capital is the simplest form of financing and is usually the most cost-effective because there is no interest to pay. The cost of financing projects using inhouse capital is the rate of return that could be achieved by using that capital for other alternatives. Insufficient capital and taking on all the project risks are two drawbacks to using in-house capital.

- Loans

Borrowing funds for projects can be financially beneficial if the cost of borrowing is low enough for the life of the project. All the project risk is with the organization because the loan will still need to be repaid even if the project does not achieve the expected savings.

- Leases

Leasing options include capital leases and operating leases. These arrangements allow an organization to pay for equipment in installments with various conditions.

- Performance contract

A performance contract is an agreement between an organization and an energy services company (ESCO) whereby the ESCO finances the project and the organization pays the ESCO a fee that is less than the value of the energy savings. Performance contracts enable an organization to reduce or almost eliminate project risk.

8.6.9. Energy Performance Contracts

An energy performance contract is an agreement between an organization seeking to reduce its energy costs and an energy services company (ESCO) that designs, builds, operates, and maintains equipment to achieve reduced energy costs. The ESCO will generally arrange finance for the capital investment, and the organization will pay for the project from the energy savings achieved. At the end of the contract, the full benefits of the energy savings are retained by the organization. A lender that provides the necessary capital is often a party to the energy performance contract and will carefully evaluate the project’s risks, such as the ability of the ESCO to achieve the savings and the organization to make payments. Utility companies may also be stakeholders if they offer a rebate to the ESCO for certain equipment or demand response participation.

8.6.10. Energy Performance Contract Advantages and Disadvantages

Energy performance contracts enable an organization to improve its energy performance by implementing energy conservation measures without making a significant initial investment. The ability for an organization to carry out a large-scale retrofit project without using their own capital or obtaining a loan is one of the major benefits of a performance contract. Other benefits include lower risk of failure because the contractor takes on performance risk, and the ongoing maintenance of the equipment will be included in the contract. The disadvantages of a performance contract include entering a long-term contract that will mean some control is relinquished to the contractor in terms of facility operations and further upgrades to building energy services. The cost savings achieved by the project will be shared with the contractor for a significant period of time, so the overall value of savings will be reduced compared to other means of in-house financing. The performance contract will also be a more complex process that will require time and expertise to manage throughout the contract.

8.6.11. Energy Performance Contract Structures

There are a variety of contractual arrangements that an energy services company (ESCO) will use to reduce a customer’s energy costs:

- Guaranteed savings

The ESCO designs and implements a project and guarantees the amount of energy savings that will be achieved. The ESCO accepts the performance risk for the project, so any savings shortfall will be met by the ESCO. The ESCO may facilitate financing arrangements, but the customer will contract directly with a lender.

- Shared savings

The ESCO designs, finances, and implements a project, and the energy savings are shared between the customer and the ESCO for a specified period. The amount of savings is not guaranteed, and contracts may be longer than needed for guaranteed savings, so the ESCO can recover the investment costs.

- Chauffage

An ESCO will take over the operation and maintenance of equipment and charge fees to provide specified services, such as cooling and heating. Any investment in equipment upgrades will be made by the ESCO, but ownership remains with the customer.